When lenders consider making a loan to your business, they want to be assured the loan will be repaid on time. The type of debt already on your books will be a factor in that decision.

Let’s look at the different types of debt, both business and personal, and see how they can affect an application for a business loan.

The 4 Most Common Types of Debt

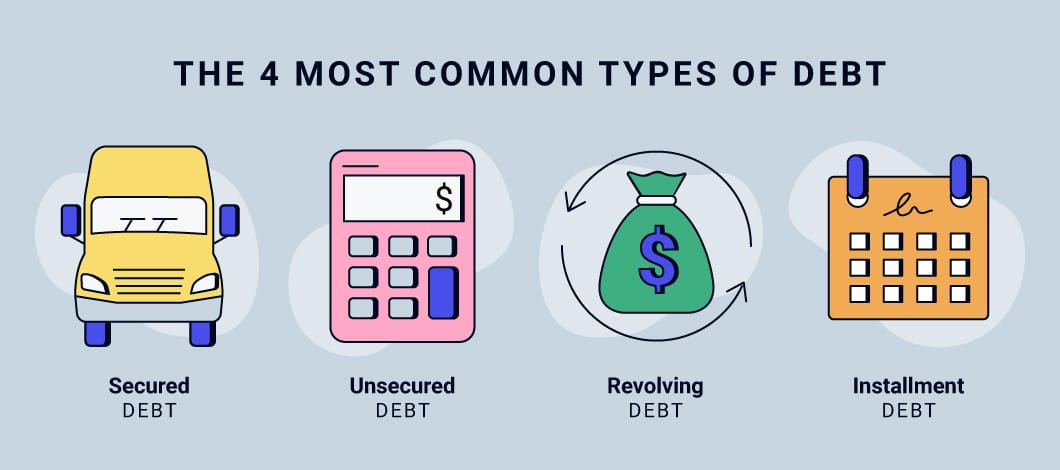

1. Secured Debt

Loans backed by specific collateral are considered secured. If the borrower defaults, the lender has the right to repossess and sell the underlying assets and apply the proceeds to the loan balance. Examples of secured debt include equipment loans and term loans.

For example, an equipment loan to purchase a utility truck would have payments spread over several years and would be paid out of the company’s cash flow. The truck would be the security for the loan.

Another example is a loan used to buy a new computer system to manage accounts receivable and inventory. This would also be a term loan with payments coming out of the company’s cash flow.

2. Unsecured Debt

For unsecured loans, which do not involve collateral, banks require a healthy balance sheet. Applicants should also have a comfortable debt service coverage ratio, which measures a company’s ability to pay all of its debt obligations out of its operating income.

The strength of a balance sheet is measured by the company’s debt-to-equity ratio, which is found by dividing its total debt by its shareholders’ equity. For small businesses, a good ratio is a minimum of $1 or less in debt for $1 in equity.

Banks look for this debt-to-equity ratio to provide a margin of security in the case of loan defaults. This ratio becomes especially important when a large portion of a company’s assets are already pledged as collateral for secured loans.

An owner’s guarantee is helpful in receiving unsecured loans from lenders because, in the case of default, the lenders do not have any specific assets to attach and must rely on any proceeds being left from a total liquidation of the business for repayment of their loans.

Examples of unsecured debt include certain loans and financing products (e.g., merchant cash advances), medical bills and most credit cards.

3. Revolving Debt

Revolving debt refers to the balance from revolving credit, another type of debt financing. These types of debt often have variable interest rates and variable payment dues. Borrowers can access funds again and again as they pay down their outstanding balance. Credit cards and lines of credit are the most common examples of revolving debt. Most credit cards are an example of unsecured revolving debt, while home equity lines of credit are examples of secured revolving debt.

In terms of how this type of debt affects your loan applications, lenders are interested in how you’re managing your credit limits. Are they maxed out, or is utilization at a manageable level (i.e., no more than 30%)?

For instance, high credit card payments, even at minimum amounts, can lead to a high debt-to-income ratio. If lenders see that you have a lot of credit card debt with high payments, they will have more concerns about how you will handle your company’s debt obligations.

On the other hand, low credit card debt is more reassuring to lenders. In the worst case, you could use credit cards to make payments if the business was not generating enough cash flow on its own operations.

4. Installment Debt

Installment debt can be secured or unsecured. However, it’s often a type of long-term debt in which the borrower pays fixed installments of principal and interest for the loan term.

Payments may be due monthly or more frequently in some cases. Typically, as you pay down an installment loan, the amount applied toward interest is reduced with subsequent payments.

Examples of installment debt include:

- Mortgages

- Personal loans

- Student loans

- Vehicle loans

How Different Types of Debt Affect Credit Scores and Loan Access

Regardless of the type of outstanding debt you have, a high credit score will boost your chances of getting a business loan, while a low score will increase lenders’ concerns. Additionally, making on-time payments on any type of debt will improve your credit score and strengthen your guarantee in the eyes of the lender. Therefore, it makes sense to work on your own credit status to strengthen your guarantee for business loans.

Good Debt

As a rule, if you borrow money to buy something that increases your net worth or will have future value, that’s good debt.

Mortgages

A mortgage on a home is an example of a good debt.

Over the long haul, a house is going to increase in value. At the same time, you’re paying down the mortgage, increasing the equity in your home and increasing your net worth.

A lender contemplating making a loan to your business will look favorably at your mortgage and payment history.

That said, if your mortgage is high in relation to your income, lenders could feel you’re not in a position to take on additional payments if you had to assume your business’s loan payments.

A lender could also be looking at the equity in your home as additional collateral. For example, a 10-year-old mortgage would be looked on more favorably in terms of collateral than a new mortgage with little equity.

Student Loans

Student loans are another type of debt category that is considered “good,” and it can be another way to strengthen your credit history if you’re making payments on time. In addition, lenders would look favorably on someone who used these loans to pay for a better education.

Bad Debt

Borrowing money to buy something that starts losing value the minute you buy it is an example of bad debt. Unfortunately, that includes many staples of modern life, such as cars and clothes.

Credit Cards

Having a few credit cards is both good news and bad news. When managed properly, they can be a good sign to lenders that you know how to responsibly manage your finances. That’s a plus when you’re asked to guarantee a business loan. But, it’s a negative if you’re overextended.

Auto Loans

This is another type of loan that can be viewed as good debt or bad debt. A car’s value starts to depreciate the day it leaves the dealer’s lot.

Of course, most people need a car to get to work and aren’t able to afford to pay for a car in full. The point is to use common sense when taking out a car loan and make a purchase you can afford. (Some experts suggest car buyers can afford a car they can put 20% down on, pay over 4 years and spend no more than 10% of their monthly income on, known as the 20/4/10 rule.)

On the positive side, a car loan with reasonable payments made on time will improve your credit score and strengthen your guarantee for business loans.

Analyzing Your Types of Outstanding Debt

The different types of debt, both business and personal, represent opportunities to improve a company’s credit standing in the eyes of potential lenders. It’s important to understand how these types of debt affect applications for business loans. Once you understand the influence of different debts, you can address them and improve them to your advantage.

Keep in mind, as with business ratios, lenders will look at your personal debt service coverage ratio, the ratio of your current fixed debt payments to your income. Additionally, if you’re a small business owner seeking to take on a new type of company debt, lenders will likely require you to provide a personal guarantee because, in reality, you and the business are the same entity.